NPS Vatsalya

NPS Vatsalya

NPS Vatsalya is a pension scheme focused on minors and is designed for parents aiming to secure their children's future.

Features

NPS Vatsalya will allow parents to save for their children’s future by investing in a pension account and ensure long-term wealth with the power of compounding. NPS Vatsalya offers flexible contributions and investment options, allowing parents to make investment of ₹1,000 annually in the name of the child, thus making it accessible to families from all economic backgrounds.

This new initiative is designed to start early in securing financial future of children, marking an important step in India’s pension system. The Scheme will be run under the Pension Fund Regulatory and Development Authority (PFRDA).

The launch of NPS Vatsalya highlights the Government of India's commitment to promote long-term financial planning and security for all. It’s a big step toward making India’s future generations more financially secure and independent.

Documents Required

- KYC of Guardian shall be carried out by submitting Proof of Identity and Address (Aadhaar, Driving License, Passport, Voter ID card, NREGA Job Card, National Population Register)

- Date of Birth proof of the Minor (Birth certificate, School leaving certificate, Matriculation Certificate, PAN, Passport)

- NRE / NRO Bank Account (solo or joint) of the minor in case the guardian is NRI.

Investment Choices

- Default Choice: Moderate Life Cycle Fund -LC-50 (50% equity)

- Auto Choice: Guardian can choose Lifecycle Fund - Aggressive -LC-75 (75% equity), Moderate LC-50 (50% equity) or Conservative-LC-25 (25% equity)

- Active Choice: Guardian actively decides allocation of funds across Equity (upto 75%), Corporate Debt (upto 100%), Government Securities (upto 100%) and Alternate Asset (upto 5%).

Withdrawal, Exit and Death

- Withdrawal up to 25% of contribution after lock-in-period of 3 years allowed for education, specified illness and disability. Max three times.

- Upon attainment of age of 18 years, Seamless shift to NPS Tier — I (All Citizen)

- Exit allowed on attainment of 18 years of age

- Corpus more than Rs. 2.5 Iacs: 80% corpus is utilized for purchase of annuity and 20% can be withdrawn as lump sump

- Corpus less than or equal to Rs. 2.5 Iacs: entire corpus can be withdrawn as a lumpsum.

- On death, entire corpus would be returned to the guardian.

Want to know more about NPS Vatsalya? Check out our list of Frequently Asked Questions for answers to your queries

NPS Vatsalya is a contributory pension system under the National Pension System (NPS) . Its objective is to create a pensioned society and encourage the empowerment of children by inculcating the habit of saving for retirement from an early age.

NPS Vatsalya is open to all citizens of India who are under the age of eighteen years. The account will be opened and operated by the guardian on behalf of the minor.

Opening a NPS Vatsalya account provides the child with a head start on saving for retirement and offers valuable financial lessons from an early age. It instills the importance of financial planning and discipline, which can benefit the child throughout their life.

- The account is opened by the natural or legal guardian in the name of the minor.

- The minor is the sole beneficiary of the account.

- A unique Permanent Retirement Account Number (PRAN) is issued in the minor's name.

- The account is operated by the guardian for the exclusive benefit of the minor until they reach the age of majority (18 years).

The NPS Vatsalya account can be opened online through:

Federal Bank website (www.Federalbank.co.in) -> Personal -> Products -> National Pension System -> “Open NPS Online” link

- The KYC norms applicable to the guardian must be in accordance with the standards stipulated by PFRDA.

- In the case of a court appointed legal guardian, a copy of the court order regarding the appointment of the Legal Guardian must be submitted along with the KYC documents.

For the minor, the proof of date of birth is required. Acceptable documents include:

- Birth certificate of the minor

- School leaving certificate / Matriculations issued by Higher Secondary Board of respective states, ICSE, CBSE, etc.

- Passport of the minor

- PAN

- The bank account details of the minor or a joint account with the minor are not mandatory for opening the account for Indian residents but will be required at the time of partial withdrawal or exit before the age of 18.

- For non-residents, details of NRE or NRO account are mandatory.

- The account will continue to be operational and will be seamlessly transitioned into a NPS -Tier 1 Account under the All Citizen Model.

- Upon transitioning, the features, benefits, and exit norms of the NPS-Tier I for All Citizen Model will apply.

- A fresh KYC of the subscriber must be carried out within three months of reaching majority. Contributions to the NPS Tier1 Account will be allowed after the submission of fresh KYC.

- The minor must be a citizen of India.

- The guardian can be a Non-Resident Indian (NRI) or Overseas Citizen of India (OCI).

- A separate form is applicable for guardians who are NRIs or OCIs.

- A bank account (NRE or NRO) is mandatory when the guardian is an NRI or OCI.

No, the guardian becomes the nominee under the scheme.

The guardian can open a single account (per child) for the minor.

Yes, a guardian who is a NPS subscriber can open a NPS Vatsalya account in the name of the minor.

- The minimum contribution is Rs 1000 per annum, with no upper limit on the maximum contribution.

- The initial contribution required for enrollment under the scheme is Rs 1000.

A subscriber can contribute through any of the following modes:

- Physical mode: By visiting any registered service provider (PoP) and depositing a cheque/cash along with the NPS contribution slip.

- Online mode:

- Online facility provided by PoPs.

- eNPS platform of NPS Trust.

All choices available under the NPS All Citizen model are also available for NPS Vatsalya, including:

- Choice of CRA (Central Recordkeeping Agency): From the registered CRAs with PFRDA.

- Choice of Pension Fund (PF): From the registered PFs with PFRDA.

- Choice of Allocation of Funds:

Auto Choice:

- Conservative Life Cycle Fund (LC25)

- Moderate Life Cycle Fund (LC50) – Default

- Aggressive Life Cycle Fund (LC75)

Active Choice:

- Equity (E) – Maximum 75%

- Corporate Bonds (C) – Up to 100%

- Government Securities (G) – Up to 100%

- Alternate Assets (A) – Maximum 5%

The contributions made by the subscriber are invested according to the choices (Pension Fund and Asset allocation) exercised and recorded with CRA, in line with the investment guidelines prescribed by PFRDA for each asset class:

- Asset Class E – Equity shares of Top 200 companies under NSE/BSE in terms of market capitalisation.

- Asset Class C – Corporate Bonds/Debentures that are listed and rated not below A.

- Asset Class G – Government securities and State Development Loans.

- Asset Class A – Alternate Assets. For detailed investment guidelines, refer to the Circulars Section of the PFRDA website.

The performance of your NPS investments is available in the Statement of Transactions, which can be accessed online through the subscriber web login or mobile app. Periodic statements are sent by the CRA to the registered email ID of the subscriber, and a physical statement for the financial year is sent to the correspondence address of the subscriber.

The charges under the NPS Vatsalya account are the same as those for the NPS Tier I for the All Citizen model.

Subscribers can access their Pension Account through:

- Physical mode: By visiting their service provider (PoP).

- Online mode: Using the login credentials provided by CRA in the Account Opening Kit.

- Partial withdrawals from your NPS Vatsalya account are allowed to address contingency situations. The reasons/conditions for partial withdrawal include:

- Education of the minor subscriber

- Treatment of specified illnesses of the minor subscriber

- Disability of more than 75% of the minor subscriber

- A maximum amount of up to 25% of contributions (excluding returns) can be partially withdrawn.

- This facility is available on a declaration basis after a minimum of 3 years from the date of account opening.

- The Partial withdrawal can be made maximum three times till subscriber attains 18 years of age.

- The subscriber can exit on attainment of age of 18 years.

- On such exit, at least eighty percentage of accumulated corpus available in the account must be utilized for purchase of annuity and remaining balance shall be paid in lump sum.

- In case, the accumulated pension wealth available in the account is equal to or less than a two lakh fifty thousand, or purchase of annuity is not available from empaneled Annuity Service Providers (‘ASPs’), the subscriber shall have option to withdraw the entire accumulated pension wealth.

- In the event of the minor subscriber's death, the entire accumulated corpus to be paid to the guardian.

- If the guardian registered under the account dies during the account's subsistence, another guardian must be registered on behalf of the minor subscriber by submitting the KYC documents as specified by the PFRDA from time to time.

- In case of death of both the parent, the legally appointed guardian can continue the account with or without making contributions to the account, and upon attainment of 18 years of age, the subscriber can exit from the scheme.

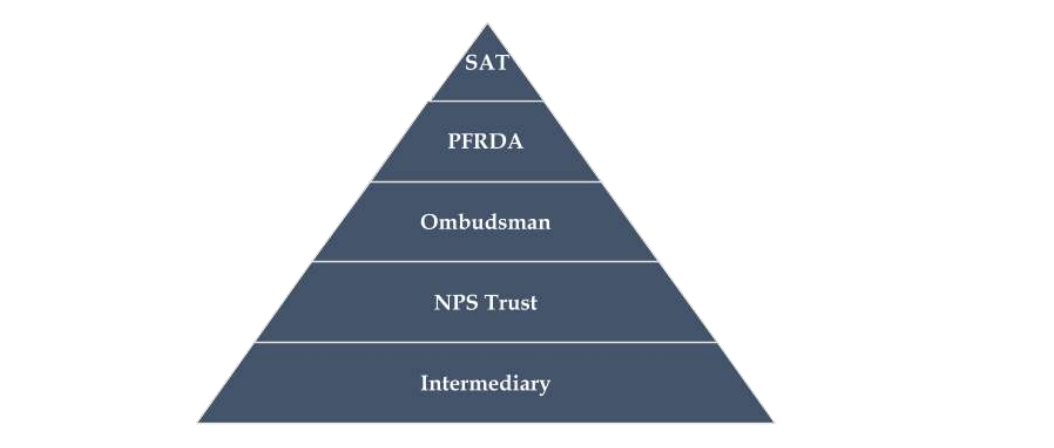

- For resolving subscriber grievances, the Authority has notified the PFRDA (Redressal of Subscriber

- Grievance) Regulations, 2015 and an online platform ‘Central Grievance Management System (CGMS)’ has been hosted for subscriber to lodge grievance online by logging to his/her NPS account.

- A complaint/grievance has to be resolved by the intermediary concerned as early as possible within a maximum period of 30 days of the receipt of the complaint.

- If a subscriber is not satisfied with the resolution provided, he/she can escalate his grievance to the next higher level for resolution and the escalation matrix is as under: